Funding

Solutions

You Can

Bank On

Get access to the capital you need to grow and scale your business. Rates as low as 0%.

Get pre-approved today!

This does not impact your credit.

I agree to the terms and conditions and privacy policy. Furthermore, I grant permission for Impruvu LLC to communicate through the contact details provided in this form. Reply STOP to unsubscribe from SMS at any time.

Client Testimonials

Fund Your Business.

Fund Your Life.

We specialize in personal and business funding with more than 40 different funding programs.

Business Line of Credit

Leverage a revolving line of credit and only pay for what you need. Access funds at your pace, as your business needs

0% Business Credit Stacking

Launch your business with the confidence of multiple 0% interest accounts. Enjoy cash accessibility with revolving credit at a 0% interest rate.

Asset Based Lending

Unlock the power of your company’s assets. Leverage your inventory, equipment, or receivables into the funds you need to grow and sustain your business operations.

Long Term Business Loans

Experience the reassurance of a traditional process with lower payments spread over a longer term.

Short Term Business Loans

Unlock quick access to funds for any business expenses. Your solution to fast, convenient financing when time is of the essence.

Personal Loans

Secure up to a five-year personal loan to manage your credit card balances, enhance your score, and qualify for 0% funding.

Bring Opportunity to Everyone

Our team of professionals is specifically trained to secure the best available funding at the lowest rates. We are available every day to help you get started.

01

Pre-approval Form

02

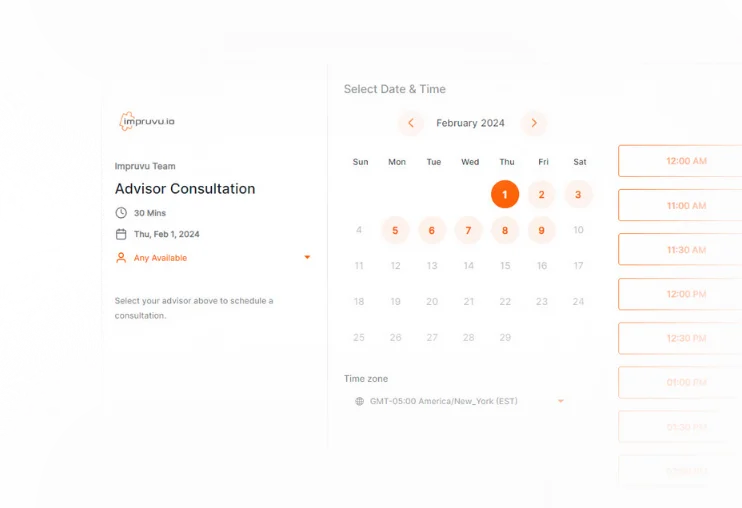

1-on-1 Consultation

03

Digital Onboarding

04

Funding Process

A Better Funding Experience.

Customized funding solutions and consultations to help achieve your growth goals.

Jon Stalcup

4h ago

@lvan, just wanted to share some great news! We've been approved for the $155k at 0% interest. Your insight into our financial strategy was invaluable. Thanks for guiding us through the application process. Looking forward to the next steps!

Ivan Molina

3h ago

That's fantastic, @Jon! Congratulations on the approval. Let's schedule a meeting to discuss how to best allocate these funds in line with your business growth objectives. Also, I have a few ideas about optimizing your cash flow management with this new capital.

Alex Green

30m ago

@lvan, just caught up with Jordan about the funding news incredible work! This opens up so many opportunities for us.

Can we set up a time to go over a detailed investment plan? I'm particularly interested in exploring how this can accelerate our expansion plans.

Consultation Notes

September 10, 2023 3:23PM

Recommended Steps to Improve

Qualifications for Funding:

- Lower your credit card utilization on the individual accounts that are significantly over the stipulated 30% utilization rate.

- Avoid opening new credit accounts or incurring hard inquiries to keep your applications within the desired range.

Jon Stalcup

4h ago

@lvan, just wanted to share some great news! We've been approved for the $155k at 0% interest. Your insight into our financial strategy was invaluable. Thanks for guiding us through the application process. Looking forward to the next steps!

Ivan Molina

3h ago

That's fantastic, @Jon! Congratulations on the approval. Let's schedule a meeting to discuss how to best allocate these funds in line with your business growth objectives. Also, I have a few ideas about optimizing your cash flow management with this new capital.

Alex Green

30m ago

@lvan, just caught up with Jordan about the funding news incredible work! This opens up so many opportunities for us. Can we set up a time to go over a detailed investment plan? I'm particularly interested in exploring how this can accelerate our expansion plans.

Consultation Notes

September 10, 2023 3:23PM

Recommended Steps to Improve

Qualifications for Funding:

- Lower your credit card utilization on the individual accounts that are significantly over the stipulated 30% utilization rate.

- Avoid opening new credit accounts or incurring hard inquiries to keep your applications within the desired range. If this information is accurate and thereare no recent accounts missing from this report, you are in a strong position regarding your credit score and lack of recent derogatory items or hard inquiries.

Streamline effective funding.

We make getting the funding you need quick and easy with a simple 4 step process.

Quick Prequalifying

Experience a streamlined prequalification process, ensuring you quickly find the right products or services tailored to your unique business needs.

Easy Onboarding

Our user-friendly onboarding system simplifies your journey, allowing you to effortlessly integrate our products and services into your business operations.

1-on-1 Consultations

Benefit from personalized, one-on-one consultations with our expert advisors, dedicated to understanding and addressing your specific business challenges and goals.

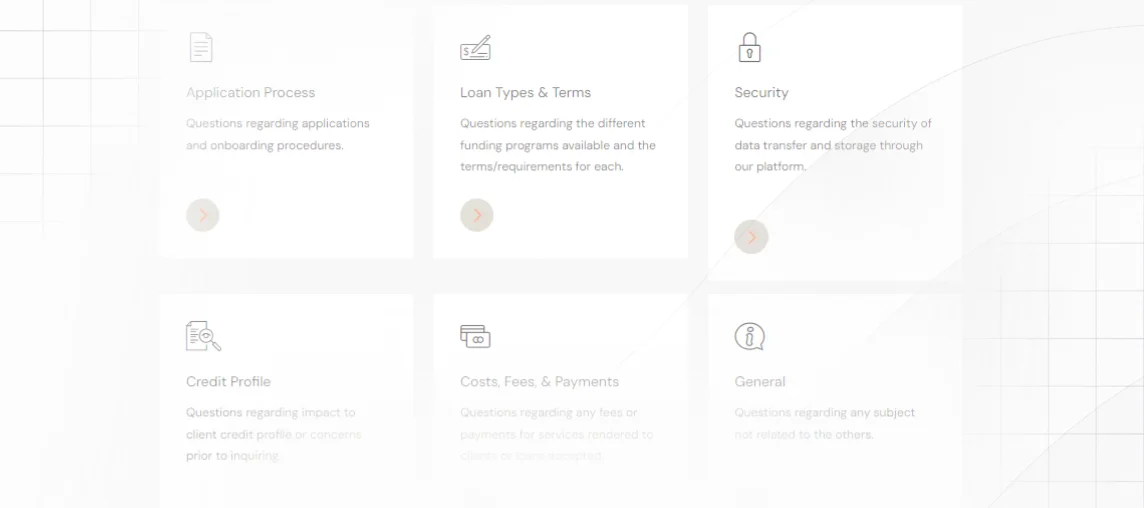

Guided Solutions

Access our comprehensive help center and FAQs, along with tailored educational materials, designed to guide you through every step of utilizing our solutions effectively.

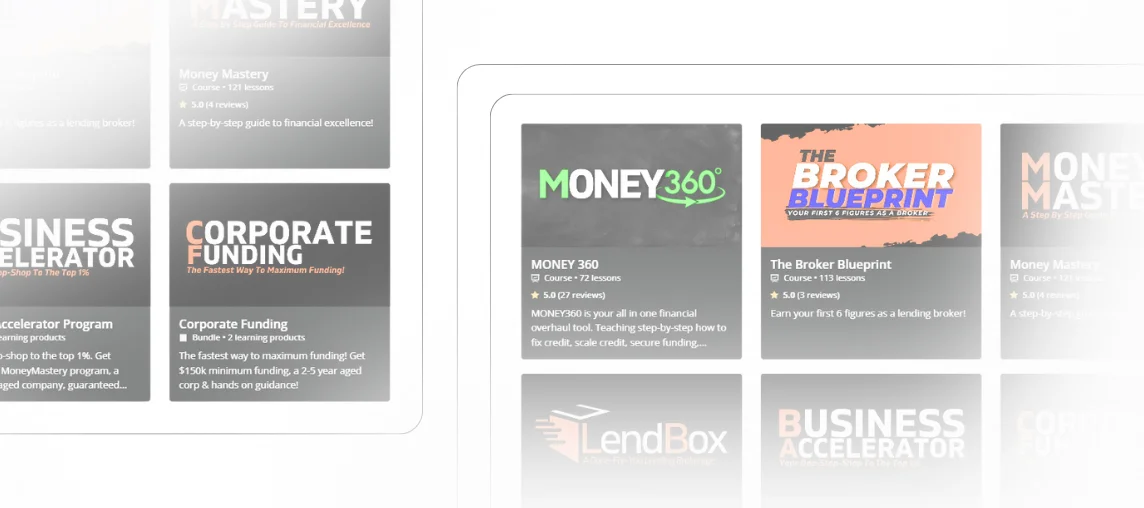

Ongoing Education

Enhance your business and financial acumen with our extensive range of educational courses, constantly updated to keep you ahead in a dynamic business world.

Copyright © 2024 Impruvu LLC. All Rights Reserved.